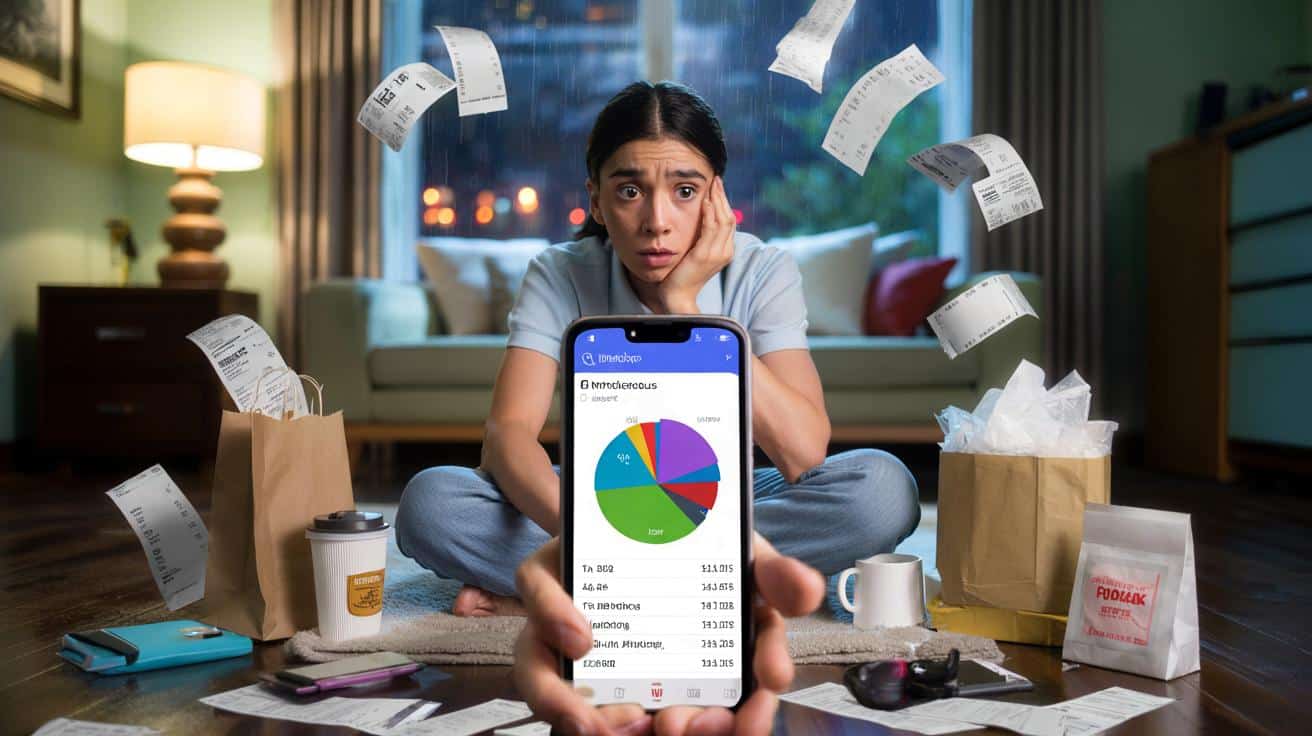

On a rainy Tuesday, I was sitting on the floor with my bank app open, receipts spread out like confetti.

Rent, groceries, gas, nights out — all highlighted, neatly categorized, nothing dramatic.

And yet my balance was quietly bleeding out every month, like a slow leak I couldn’t find.

I’d cut the streaming services, said no to a couple of dinners, downgraded my phone plan.

Still, the numbers didn’t budge.

That day I scrolled down one more time and saw a line that made me sit up straight: “Other / Miscellaneous: 27%”.

I wasn’t overspending, I realized.

I was underestimating an entire category.

The silent budget killer hiding in “miscellaneous”

We love clean budgets with tidy names: rent, food, transport, fun.

Everything else? It gets lazily dumped into “miscellaneous” or “other”, like a junk drawer for our money.

Looks harmless. Two or three small things, right?

Except that pile of “small things” grows teeth.

It’s the pharmacy run, the last-minute gift, the coffee for a friend, the parking meter, the notebook you forgot you needed.

None of them feel like overspending in the moment.

Then you open your statement and realize this one vague line is quietly larger than groceries.

That’s when the story changes.

Think about last month.

Maybe you grabbed a taxi because it was raining, ordered a quick takeaway on a busy night, bought a phone charger, donated a bit to a fundraiser, replaced a broken mug.

Individually, these are “nothing” purchases.

You barely remember half of them by the weekend.

Yet together they’re the closest thing your budget has to a black hole.

One reader told me her “miscellaneous” was 35% of her monthly spending.

Another tracked her “random” category for a month and found she was spending one full extra rent payment a year on it.

The problem wasn’t that they were reckless — they were blind.

Here’s the strange logic at play.

We like to believe we’re rational spenders, so we focus on the big, socially acceptable categories: housing, food, transportation.

Those are the ones we negotiate, optimize, proudly brag about.

➡️ This is how to store things without overthinking it

➡️ If you feel uncomfortable being fully honest, psychology explains what your mind is protecting

➡️ “I thought effort was the answer”: why gentler habits worked better

➡️ I noticed my home stayed cleaner once I stopped cleaning certain areas so often

➡️ The habit of staying busy all the time often hides a psychological discomfort with stillness

➡️ “I didn’t realize how tense I was”: what my posture was silently doing to my body

➡️ Psychology explains why certain emotional triggers feel disproportionate but deeply real

The “other” category? That’s emotional terrain.

It’s filled with small comforts, last-minute fixes, and social obligations we feel guilty questioning.

We don’t talk about it, we don’t plan for it, and we don’t want to see how big it really is.

*That’s how a category you barely name starts quietly running your entire budget.*

Not because you’re bad with money, but because this part of your life never got a proper line of its own.

Give the “unknown” a name and a number

The most effective move is almost boring: rename and split your “miscellaneous”.

Open your banking app or spreadsheet and scroll to that catchall zone.

Instead of one vague bucket, carve it into 3–5 mini-categories that feel real to your life.

For example: “Little comforts”, “Social & gifts”, “Household & fixes”, “Health & pharmacy”.

The names matter more than we think because they force your brain to pay attention.

You’re not spending on “random stuff” anymore; you’re choosing between comfort, generosity, and repairs.

Once those lines exist, give each one a rough monthly cap.

Not perfect, not final.

Just a number that makes you go, “Okay, that’s reasonable… I think.”

Here’s the part where most people trip: they try to be perfect from day one.

They slash their “random” spending in half, set strict rules, and promise they’ll log every cent.

Week two, life happens, they miss a day, and the whole thing collapses.

Let’s be honest: nobody really does this every single day.

A kinder approach works better.

Track your “new” categories for one month without judging them.

Just observe.

You might notice that “Social & gifts” is way higher than you thought, while “Household & fixes” is pretty tame.

That’s not a failure.

That’s your money finally telling you the truth about your life.

Sometimes the money story isn’t “I’m terrible with cash”, it’s “I never gave myself permission to see the full picture”.

Now, put that picture in a simple, visual box your brain can’t ignore:

- Step 1: Rename “Miscellaneous” into 3–5 real-life categories (comforts, social, fixes, health).

- Step 2: Track them for 30 days with zero judgment — pure curiosity.

- Step 3: Adjust each cap slightly next month, not drastically.

- Step 4: Keep one small “true misc” line for genuine one-off surprises.

- Step 5: Review monthly and change the labels if they don’t fit how you actually live.

The list lives better on your phone than in your head.

You don’t need discipline as much as you need a simple map you’ll actually look at.

When the “problem” wasn’t overspending at all

There’s a quiet shift that happens once you stop treating this as a moral failing and start treating it as data.

You realize you weren’t a disaster with money — you were just running on an outdated story.

The real issue wasn’t lattes or takeout; it was a category that didn’t exist yet.

Sometimes the healthiest move isn’t cutting, it’s acknowledging.

You might decide that yes, you really do value small daily comforts and you’re willing to give them an honest line in your budget.

Or that gifts and social moments matter so much to you that they deserve planning, not guilt.

The leak shrinks the moment it has a name.

From there, every choice feels a bit more intentional, a bit less like mystery quicksand.

| Key point | Detail | Value for the reader |

|---|---|---|

| Identify the hidden category | Stop hiding expenses under “miscellaneous” and rename them into real-life groups | Instant clarity on where money is actually going |

| Track without judgment | Observe spending for 30 days before changing anything | Reduces shame and builds a more accurate picture |

| Set gentle limits | Assign realistic caps to each new category and tweak monthly | Creates control without feeling deprived or punished |

FAQ:

- What if my “miscellaneous” is bigger than rent?

You’re not alone. Treat it as a signal, not a crisis. Break it into 3–5 categories and see which one is carrying most of that weight. Start adjusting the biggest one by 10–15%, not by half.- Is it bad to have a “random fun” line in my budget?

No. A realistic budget usually needs a “chaos” line. The goal isn’t to delete it, but to keep it small and honest, not a dumping ground that hides patterns from you.- How do I track this if I hate spreadsheets?

Use your banking app’s tags, a simple notes app, or a basic budgeting app. The method matters less than choosing something you’ll still use three weeks from now.- What if my income is too low — isn’t this just math?

Sometimes the numbers truly don’t stretch, and that’s real. Even then, understanding your hidden category helps you decide where *not* to feel guilty and where small changes can free a bit of breathing space.- How long before I see a difference?

Many people notice a shift in 30 days, and a clear pattern in 60–90. The “aha” moment usually comes when you realize this wasn’t about being careless — it was about finally seeing the category that was there all along.